By Michael Gold, CFP®, MBA Founder & CEO – Wealth Advisor

Do you know how much money you need to ensure you do not outlive it? Many people naturally wonder how much money will be needed after retirement. One excellent book to help you with this wonder that I recommend is Rewirement by Jamie Hopkins.

The author gives a great overview of the major decisions we all need to make when it comes to retirement planning. Hopkins makes one important distinction in the beginning: Instead of focusing on savings, think about cash-flow. In other words, set your sights first on the retirement income planning you will need to support your desired lifestyle when you are no longer working and build your retirement plan from there.

Hopkins also asserts (and I agree with him) that there is no “magic number,” as the specifics depend on your retirement goals and your situation. However, there are some simple and consistent practices that will help to pursue clarity about what your retirement finances need to look like.

Identify Retirement Expenses

To decide how much cash-flow you will need in retirement, remember that retirement consists of different phases. Most people tend to think about traveling the world, volunteering, spending time with grandchildren, and other activities that characterize the early stages of retirement – these are your “go-go years.”

In the later stages of “go-slow and no-go years,” long-term care costs play an increasingly central role. You will likely come to depend on others for more of your needs over time and your living arrangements will likely change.

Costs will increase. You might begin to need help with cleaning, mowing the lawn and other household chores that you are accustomed to doing on your own. Medical care tends to increase with age and so do the costs associated with medical needs. It is important to purchase the appropriate levels of insurance coverage early to protect against future health and long-term care costs.

Click here to download our free guide: Managing Long-Term Care in Retirement

Retirement Income Sources

Once you have estimated your major expenses during retirement, you can think more clearly about how much income you will need each year. Most people find that the process feels clearer and more manageable when breaking down needed income into different sources.

Retirement accounts such as a pension plan or a 401(k) can provide a portion of your income, but these funds often fall short. Social Security provides additional guaranteed income. Medicare can offset your medical expenses, as well as many life insurance policies that offer “living benefits.”

If you own a home, a reverse mortgage might also provide additional income in retirement. Last, but not least, factor in any possible sources of residual income after retiring such as royalties, dividends, or other distributions from business ventures.

Key Considerations in Retirement

Several factors need to be weighed and considered when you’re doing retirement income planning.

Longevity

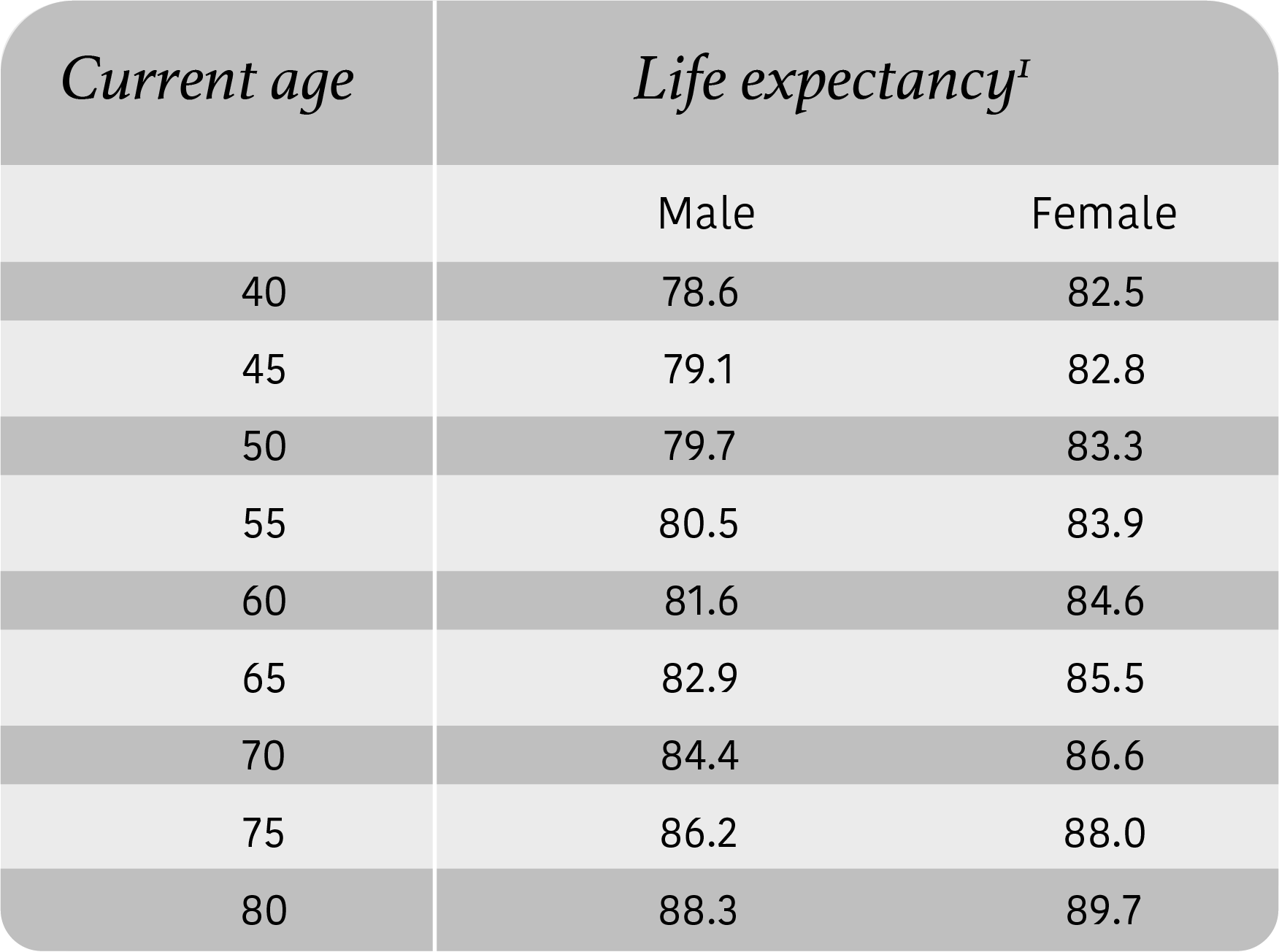

Understanding your life expectancy is important and a good place to start (see below). However, keep in mind that you may have even greater longevity than the standard life expectancy. Many people are living longer lives these days, so even if you do not think you will go the distance, it’s better to be safe than sorry and be sure to factor in longevity into your plan.

Source: Social Security Administration, 2016 Period Life Table. Please note that the Social Security Administration has temporarily suspended updates to this chart.

Inflation

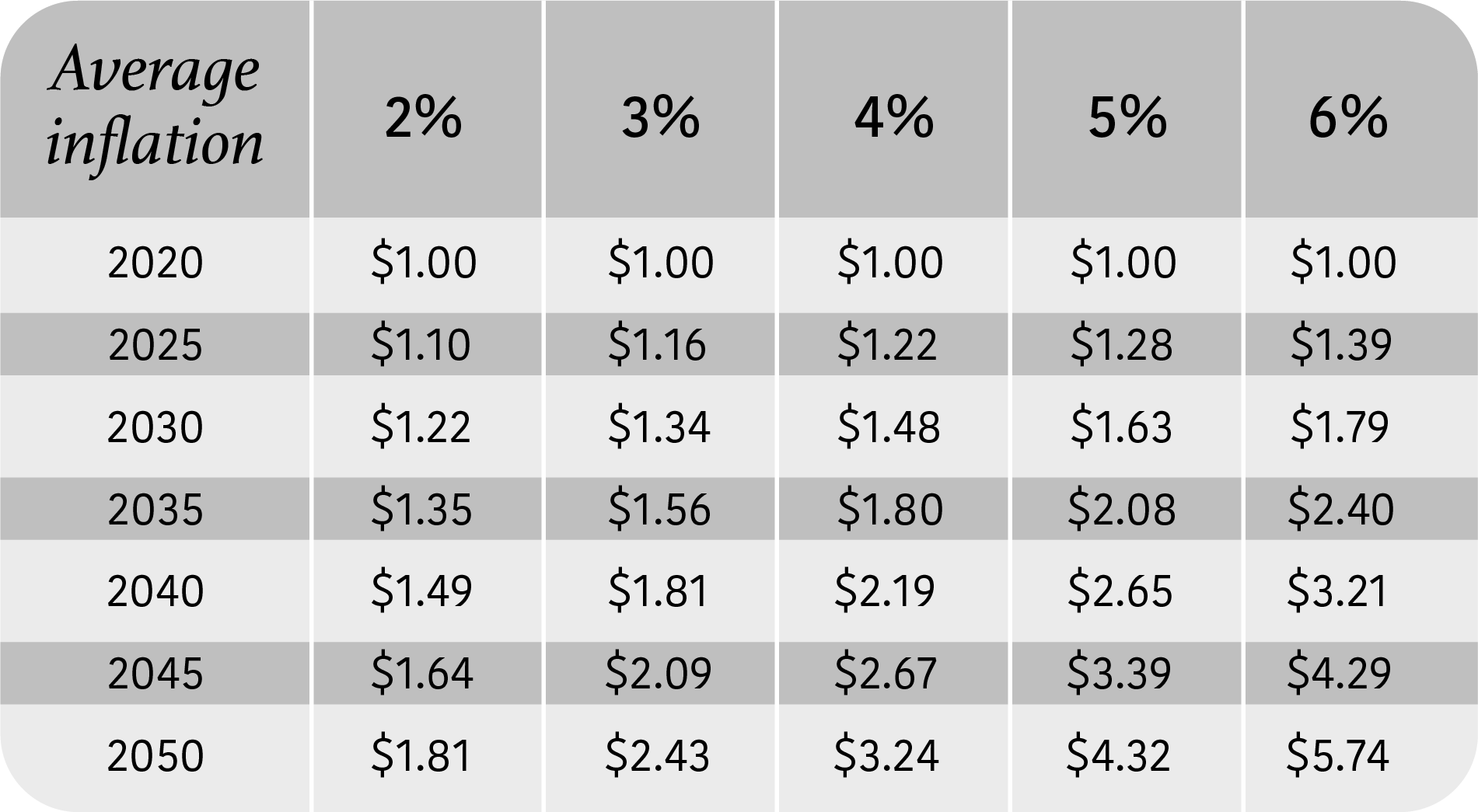

Second, is the erosion of your purchasing power. Simply put, milk, eggs and everything else you typically purchase will cost more tomorrow than it does today.

How much of an issue is this? Well, think of it this way: If your cost of living is $100,000 today and if inflation grows in the amount of 4% per year, over the next 15 years of your life or by 2035 it will cost you around $180,000 to maintain the same lifestyle as you have today.

Pretty scary stuff! Check out the chart below to see the impact of different levels of inflation on your purchasing power:

Note: For illustrative purposes only. Calculations and amounts are approximate due to rounding. Inflation has been compounded annually. This table is not intended to predict or represent any actual historical period.

Taxes

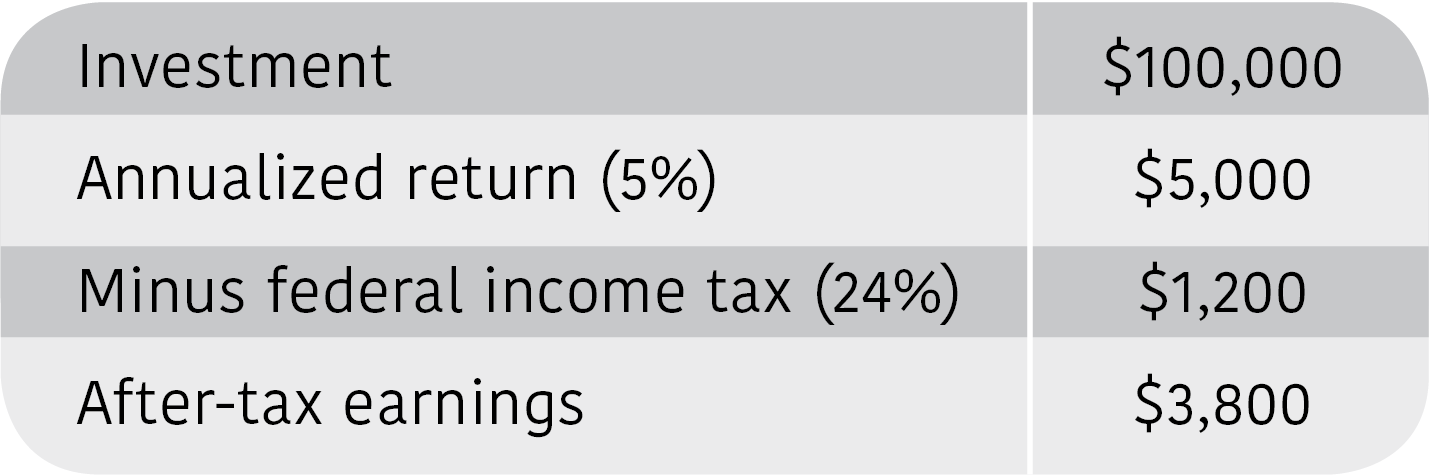

Taxes can take a big chunk out of your retirement. For example, if you have $1 Million in your IRA or 401(k) the government essentially has a claim on a third of those assets. Every dollar withdrawn will be subject to income taxes. Yikes!

Balancing Risk

Lastly, it is even possible to be too conservative with your investment strategy. In many cases, folks retire and feel it’s time to be uber-conservative and invest in a fixed income strategy to ensure their principle stays intact. Unfortunately, this does not work anymore.

People are living much longer today than in previous generations. Today there is a very good chance your retirement will last two to three decades. With that type of time horizon, the great risk lies with inflation and taxes eroding your principle from the inside like termites.

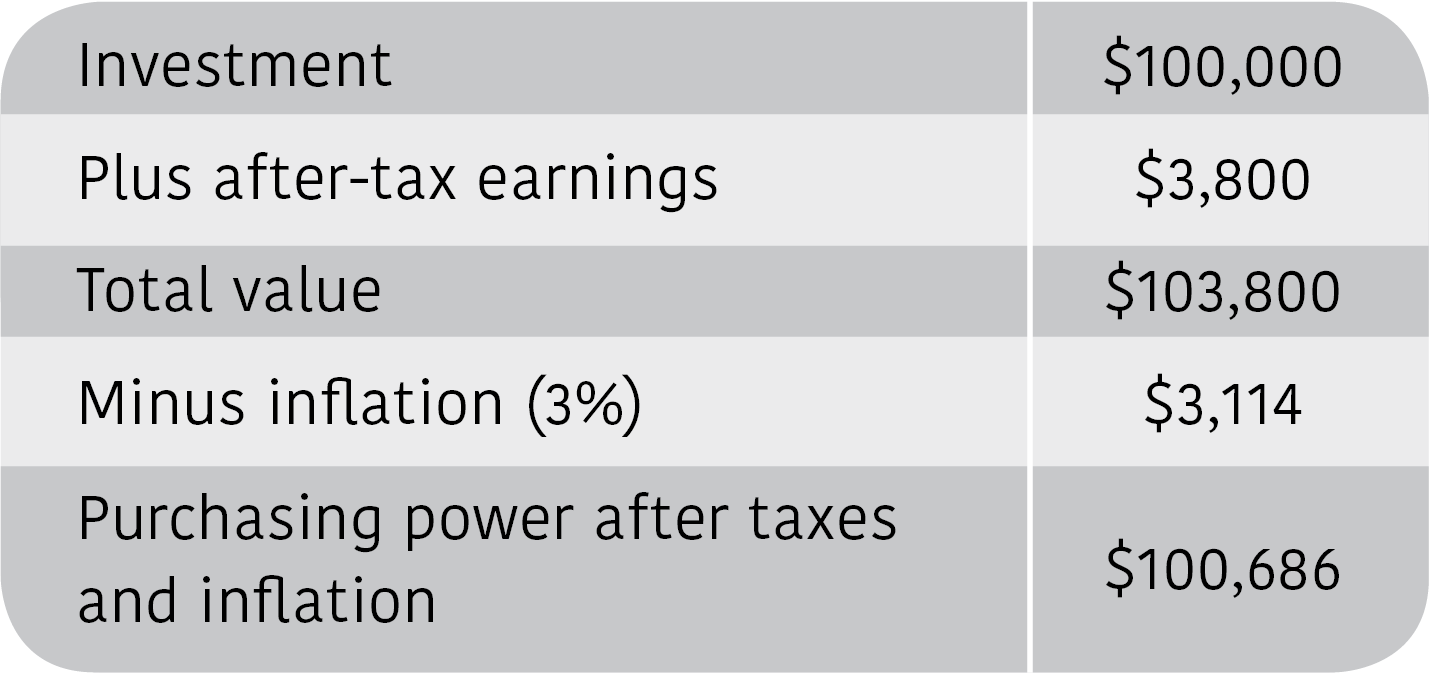

Let me illustrate this for you, (let’s use the following figures as a hypothetical scenario) let’s say you invest $100,000 in a bond that pays 5% what does your after-tax return look like?

Note: The hypothetical investment results are for illustrative purposes only and should not be deemed a representation of past or future results. Actual investment results may be more or less than those shown. This does not represent any specific product [and/or service]

Now that you have reduced your return, lets factor in a 3 percent inflation rate and see what you are left with:

Your real return in this scenario is nothing to write home about and what if inflation and taxes are higher than this?

Note: The hypothetical investment results are for illustrative purposes only and should not be deemed a representation of past or future results. Actual investment results may be more or less than those shown. This does not represent any specific product [and/or service]

Tying It All Together:

The sheer variety of investment options in retirement income planning can feel overwhelming to many people, and this is why I usually start most retirement planning conversations by getting an understanding of values.

What drives you? What do you most enjoy doing outside of work? Who are the people you like to work with? How do you envision your family life in the long term? These questions play a key role not only later in life, but they also shape the decisions you need to make right now.

When you have your long-term goals in front of you, we can envision together what your ideal retirement looks like and how much you need to provide the level of cash-flow, factoring in taxes, inflation, longevity and health care to help make your ideal vision a reality.

Ready to begin the retirement income planning conversation? Get in touch with us today to set up a complimentary initial consultation to look at your options and talk through your dreams.

Click here top Set Up Your Complimentary Consultation

About Michael

Michael Gold is the Founder and CEO, Wealth Advisor of Gold Family Wealth, an independent wealth management boutique and named one of the Top 100 People in Finance. Michael has 20 years of experience in the financial industry and has a bachelor’s degree in business and economics from the State University of New York College at Oneonta, an MBA from NYU Stern School of Business, specializing in Quantitative Finance and Leadership and his CERTIFIED FINANCIAL PLANNER™ (CFP®) credential. He serves business owners and entrepreneurs by stress-testing their financial plan to identify red flags and missed opportunities. Michael strategically outsources professionals from various fields, such as tax, insurance, retirement and trust and estate law to collaborate on potential solutions to help position his clients to pursue their desired goals.

Michael currently lives in Westport, CT. When he’s not working, you can find him spending time with his wife, Giselle, their three children, Sebastian, Aria, and Pierce, and their dog, Charly. To learn more about Michael, connect with him on LinkedIn.

___________

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Gold Family Wealth, LLC), or any non-investment related content made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Gold Family Wealth, LLC. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Gold Family Wealth, LLC is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. A copy of the Gold Family Wealth, LLC’s current written disclosure statement discussing our advisory services and fees is available upon request. If you are a Gold Family Wealth, LLC client, please remember to contact Gold Family Wealth, LLC, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services.

Investment advisory services offered through CWM, LLC, an SEC Registered Investment Advisor. Carson Partners, a division of CWM, LLC, is a nationwide partnership of advisors.

“Top 100 Magazine selections are made utilizing proprietary software, which employs an algorithm to search a variety of online resources for industry-specific terms and keywords. These resources include social media, blog posts, peer reviews, and Google indices. In addition, wealth managers must also the following criteria: 1. Registered with the SEC as a registered investment adviser or a registered investment adviser representative; 2. Not more than 1 filed complaint and never been convicted of a felony. Listing in this publication and/or award is not a guarantee of future investment success. This recognition should not be construed as an endorsement of the advisor by any client.”